Midyear Market Commentary - Second Quarter 2022

Midyear market commentary

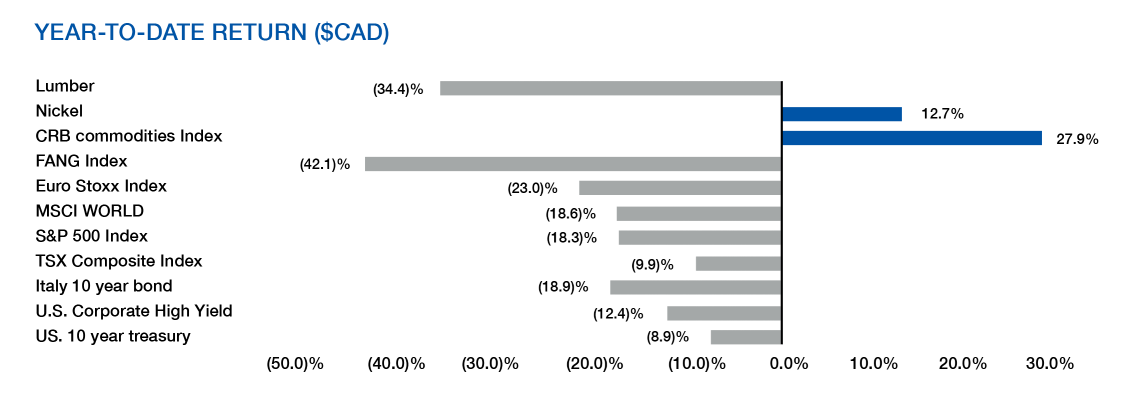

While it is never pleasant to see our portfolios fall, our style and disciplined approach have helped all of our strategies do much better so far this year. They outperformed their benchmarks between 2.1% and 7.3%, while the Canadian equity index was down -9.9%, its global counterpart -18.8% and the Canadian bond index -12,2%.

It has been a difficult start as markets faced a laundry list of concerns, notably new COVID lockdowns and economic weakness in China, Russia/Ukraine war, surging inflation, central bank tightening and increasing fears of recession.

These issues are now well understood now by the markets but at the beginning of the year, it was unclear how far inflation would rise or how aggressive the response of central banks would be. With Russia’s invasion of the Ukraine supercharging inflation and central banks determination to tame it through rate hikes and reduction of their bond holdings, the situation led to a turbulent first half in global markets. For instance:

Global equity markets lost $13T in value

The Yen plunged 15.5% against the USD

Italian bonds have had their worst rout since the Eurozone crisis

We saw widespread crypto and tech carnag

Investors looking for comfort found few safe havens as bonds had their worst half since 1988. With no relief on inflation in sight, central banks around the world are ratcheting up their plans to hike rates, causing a rapid reset of expectations and a sharp sell-off in bonds. Gold, another traditional safe haven, was also down 4%.

The only positive was in the commodity complex, where we saw the strongest rally since WW1 as crude oil experience its largest increase since 2009 and wheat and corn rose by over 20%.

In the midst of all this actions, to no one’s surprise, the FANGAM (Facebook, Amazon, Netflix, Google, Apple, Microsoft) stocks have been roiling the markets with their most recent earnings. In order to put things in context, over the course of a decade (2010-2019) the FANGAM stocks increased in collective market capitalization from $719 billion USD to $5.07 trillion, rising by more than 1791% and cumulatively representing close to 15% of the US market. These compagnies got even stronger during the first phase of the pandemic, as their business models were leverage to social distancing. Between Feb 2020 and August 2020, these companies collectively added $ 1.4 trillion USD to the market cap, rising by 45% while the overall market dropped. However, since then, their performance has lagged as their earnings fell short of expectations. Collectively, they are now down 50% on average since the beginning of the year.

We also saw severe corrections in some of the riskier assets such as the crypto currencies and NFTs, after reaching peak prices in the fall. Bitcoin, the most popular cryptocurrency has fallen by 70%. We also saw a run on the “stable-currencies” which ended up being less than stable. Lenders such as Celsius Network, Babel Finance and Vauld have suspended withdrawals. The NFT market is flatlining as well as sales continue to drop and NFT buyers vanish. According to the CryptoSlam NFT tracker, the average price of an NFT has dropped 67% in value.

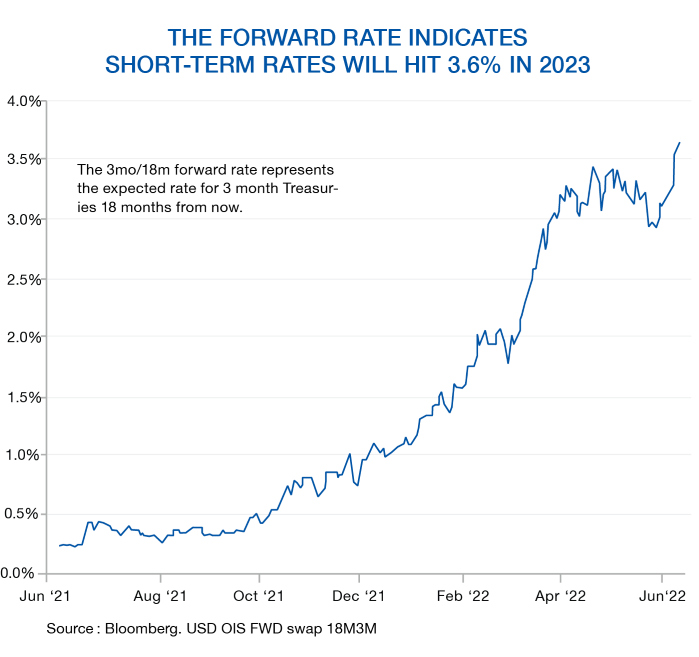

However, we are starting to see some light at the end of the tunnel. The things that were most concerning for markets at the start of the year are starting to show some change and potentially normalize. Recession fears are starting to be priced in the markets. This is most evident in the commodity space with lumber down 42% while copper, nickel and zinc are down between 20% & 25% from their peaks. With the magnitude of the expected Federal reserve tightening, as evidence by the bond market’s pricing in a Fed Fund at 3.6%, the risk of a recession is quite high. Goldman Sachs puts a risk of a recession at over 40%. The markets are now grappling with the timing of the recession and its severity, which will obviously impact corporate earnings.

Lessons from previous corrections however is that periods of panic can provide the best opportunities for long-term investors. As we focussed on companies with a prudent capital structure, generating solid profits by meeting their clients needs, and trading at attractive valuations, we expect our investment process to continue to weather the bear market. The current correction in stock prices has brought several companies that we like but were too expensive to attractive buying levels and we expect to take advantage of these opportunities in the near future.

Author(s)