At the beginning of the year, several sources of uncertainty were fueling investor nervousness. Donald Trump had just been re elected and was preparing to begin his second presidency. He had clearly expressed his intention to act forcefully on economic and immigration issues. The unpredictability of his new administration, particularly regarding trade policy, illustrated by the announcements of reciprocal tariffs made during the so called Liberation Day and the market fluctuations that followed, revived fears of a return of inflation and of a possible slowdown in the global economy.

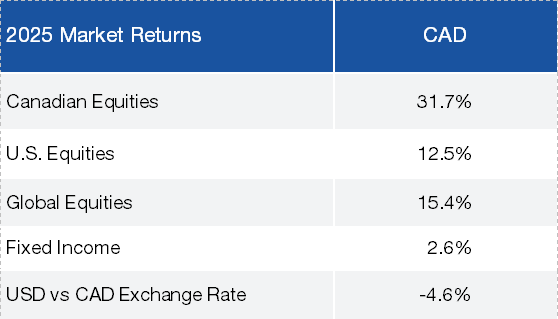

In the end, the scale of the tariffs proved to be smaller than expected, and North American central banks were able to continue lowering their policy rates. This development supported the markets, the economy, and companies in the financial sector. Furthermore, enthusiasm surrounding artificial intelligence remained widespread. Europe performed well as the valuation gap relative to the United States narrowed. In Canada, gold continued to benefit from its role as a safe haven in a context of growing geopolitical uncertainty. The result: strong returns in almost all parts of the world, particularly in Canada at 31.7 percent and in Europe at 29.1 percent.

Our portfolios produced good results this year. If not for the record performance of the gold subsector in the Canadian market, all our strategies would have outperformed their benchmarks. In last year's Third Quarter edition of To The Point, we explained why, like Warren Buffett, we refrain from investing in gold.

RETURNS ON MAJOR ASSET CLASSES (CAD)

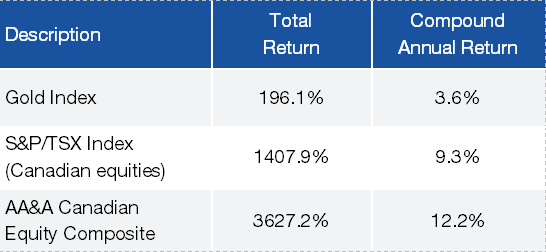

To quantify the long-term impact of this philosophy, we compared the performance of gold stocks, meaning gold mining companies, to that of the Canadian equity market and to that of our Canadian Equity Portfolio since our inception in July 1995. The following table summarizes the results. Over this period of more than 30 years, the absence of gold stocks has contributed positively to client returns.

RETURNS FROM JULY 1, 1995 TO DECEMBER 31, 2025

Gold occupies a central place in economic history because of its unique properties: scarcity, shine, malleability, divisibility, resistance to corrosion, and ease of identification. These qualities explain its use for thousands of years as both currency and jewelry. Before the development of money, trade was based on barter, but this method quickly became insufficient as societies became more complex. Humans therefore adopted rare and durable objects as mediums of exchange, with gold and silver gradually establishing themselves as universal references.

Over 2,500 years ago, the minting of precious metal coins standardized value and facilitated transactions. Later, paper notes appeared, representing a fixed amount of gold held in banks. This system, known as the gold standard, lasted until 1971, the year when currencies became fiat money. Their value has since been based on confidence in institutions and economic policies rather than on gold reserves.

Today, most transactions are digital, and cryptocurrencies represent a new phase in monetary history. At each stage, confidence has become increasingly central.

Although gold is no longer a currency, it remains perceived as a store of value. Over more than two centuries, its price has slightly exceeded inflation. In the short term however, it reacts sharply to crises. Since 2022, its rise has been driven by inflation, geopolitical tensions, uncertainty surrounding U.S. policies, and massive purchases by central banks seeking to reduce their dependence on the US dollar. When these tensions ease, the price of gold tends to stabilize.

OUR FUND RETURNS (CLASS O) AS AT DECEMBER 31 2025

Equity market valuations are very uneven. The ten largest U.S. companies now make up a record 40 percent of U.S. market capitalization. The remaining stocks, particularly value stocks and small capitalization companies, trade at multiples much closer to their historical averages.

We remain confident in the long-term return potential of the companies held in our portfolios. In addition to being profitable, they have strong balance sheets, reasonable valuations, and a robust capacity to generate cash flow. We also believe that companies as a whole will benefit in the coming decades from meaningful productivity gains resulting from the growing use of artificial intelligence.

To have an RRSP contribution included in your 2025 tax return, it must be made no later than March 2, 2026. The maximum RRSP contribution is 18 percent of earned income, up to a limit of $32,490 for 2025 and $33,810 for 2026.

Regarding your TFSA, in 2026 the additional contribution limit remains at $7,000. The total cumulative TFSA contribution room since its creation now stands at $109,000, if you were at least 18 years old in 2009 and have remained a Canadian resident since.